If you are planning to retire in 2026 or are already receiving Canada Pension Plan (CPP) benefits, you likely want to know how much money you will get each month. The answer is not the same for everyone. Your CPP payment depends on your work history, how much you earned, how long you contributed, and the age at which you start receiving your Canada pension. This guide explains everything you need to learn how the government calculates your CPP, what the average and maximum payments are for 2026, and how to use the CPP payment calculator to get your own estimate.

What Is the Maximum and Average CPP Payment in 2026?

As of January 2026, the numbers below are the official figures published by the Government of Canada. Remember, these are not guaranteed. Your actual payment may be lower or higher depending on your situation.

| Type of Amount | Monthly Amount (January 2026) |

| Maximum CPP Pension (starting at age 65) | $1,507.65 |

| Average CPP Pension (starting at age 65) | $925.35 |

Most people receive an amount close to the average, not the maximum. To get the maximum, you would need to have earned at or above the yearly maximum pensionable earnings (called the YMPE) for most of your working life, usually for about 39 years between ages 18 and 65.

How Does the Government Calculate Your CPP Payment?

The calculation uses three main facts that are needed to know before using the CPP Payment Calculator:

Your Age When You Start Your Pension

| Start Age | Impact on Monthly Payment |

| Age 65 | Full calculated amount |

| Age 60 – 64 (Early Start) | Reduced by 0.6% per month (7.2% per year) before 65 |

| Age 66 – 70 (Delayed Start) | Increased by 0.7% per month (8.4% per year) after 65 |

You can also use the CPP Planner or right time optimise at canadacalculators.ca to check what the right time is to apply for CPP.

How Much and How Long You Contributed

You must have made at least one valid CPP contribution in your life. Generally, you need contributions for at least 39 years to get the maximum. If you have fewer years, your payment will be lower.

Your Average Earnings Across Your Working Life

CPP does not use every year equally. They drop out some low-earning years to give you a fairer pension.

| Component | Calculation Rule |

| Base Component | Excludes up to 8 years of your lowest earnings (up to YMPE) |

| Enhanced Component | Uses your best 40 years of earnings |

This means if you had years when you earned very little or nothing, due to illness, unemployment, or raising children, CPP may ignore those years to boost your payment.

How to Estimate Your CPP Payment in 2026

You do not need to guess when you can use the official CPP Payment Calculator. The Government of Canada provides two free tools to help you get a reliable estimate. Quick online estimate (recommended)

- Sign in to your My Service Canada Account (MSCA).

- Go to the Canada Pension Plan section.

- Click “View my benefit estimates.”

You will see estimates for starting your pension at age 60, 65, and 70. This estimate uses your actual contribution history.

Detailed estimate of CPP Payment

Use the Canadian Retirement Income Calculator on the Canada.ca website. This tool also includes Old Age Security (OAS) and workplace pension estimates.

Situations That Can Increase or Decrease Your CPP

Even after you start receiving CPP, your payment can change. Here are the most common situations.

Working while receiving CPP (under age 70)

If you are under 70 and still working while collecting your CPP pension, you must keep contributing to CPP. Those new contributions create a post-retirement benefit, an extra monthly amount added to your existing pension for life. The government pays it automatically the following year.

Getting CPP after age 65

If you delay your pension past age 65 and keep working, CPP may use those later higher earnings to replace lower-earning years from before age 65. This can increase your monthly payment. Your contributions stop automatically at age 70.

Raising children

If you stayed home or worked less to raise young children, the child-rearing provision may remove those low-earning years from your calculation. This is automatic when you apply for CPP; you do not need to request it separately.

Disability period

If you previously received a CPP disability pension, CPP protects you. They either exclude the months you were disabled or give you credits worth 70% of your average earnings from before the disability. This increases your retirement pension later.

Divorce or separation

You and your ex-spouse or ex-common-law partner can split the CPP contributions made during your relationship. This is called credit splitting. It may increase or decrease your payment depending on who earned more.

Pension sharing with your spouse

If you are married or in a common-law relationship, you can share your CPP pension with your partner. This does not change your total household income, but it can lower your taxes by moving income from the higher earner to the lower earner.

CPP Post-Retirement Benefits

This is an important feature for anyone who works after starting their CPP pension.

- You qualify if you are under 70, receiving CPP, and still working and contributing.

- Each year of new contributions gives you a small, separate lifetime benefit.

- You do not need to apply; it is automatic.

- At age 65, you can choose to stop making post-retirement contributions if you wish. At age 70, contributions stop even if you continue working.

Step-by-Step: How to Use the CPP Payment Calculator 2026

Follow these simple steps to use the official CPP Payment Estimator:

1. Register for My Service Canada Account (MSCA). You need your Social Insurance Number (SIN) and access to your bank or CRA account for verification

2. Once logged in, find the “Canada Pension Plan” section.

3. Look for “View my benefit estimates.” You will see three numbers: starting at 60, 65, and 70.

4. Adjust the age slider to see different monthly amounts.

5. Check your statement of contributions to confirm your earnings history is correct. Report any errors to Service Canada.

If you prefer not to go online, you can call Service Canada at 1-800-277-9914 and request a paper statement of contributions.

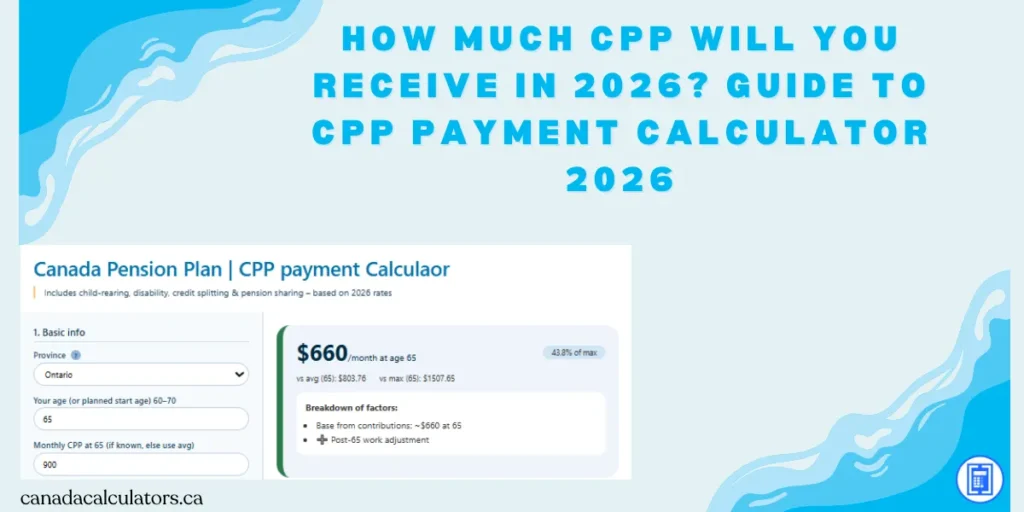

Calculate CPP Payment Without Signup: Free Accurate

Try the Free CPP Payment Calculator at CanadaCalculators.ca today, get a clear, personalized estimate of your 2026 monthly benefit in just minutes, without logging into government portals or searching through complex tables.

Whether you’re deciding when to start your pension or planning your retirement budget, this simple tool helps you understand how your contributions, age, and earnings affect your final amount. No sign-up, no jargon, just fast, reliable numbers to put you in control of your retirement planning.

FAQs: CPP Payment Calculation

1. Can I get the maximum $1,507.65 per month?

Yes, but only if you earned the maximum pensionable earnings (around $71,200 or more per year, adjusted annually) for approximately 39 years between the ages of 18 and 65. Fewer than 10% of CPP recipients get the full maximum.

2. What happens if I start CPP at age 60 in 2026?

Your monthly payment will be permanently reduced by 36% (0.6% × 60 months). If your age-65 estimate was $1,000, your age-60 payment would be $640 per month for life.

3. Does working after 65 increase my CPP?

Yes, if you delay starting your pension or if you are under 70 and already receiving CPP (through the post-retirement benefit). Any new contributions from work can increase your total retirement income.

4. How do I know if my CPP estimate is accurate?

Log into My Service Canada Account and check your statement of contributions. Make sure every year of employment is listed correctly. If years are missing, contact Service Canada with your old pay stubs or tax returns.

5. Will my CPP payment change after inflation?

Yes. CPP benefits are adjusted each January based on the Consumer Price Index. Your payment may go up slightly to keep pace with the rising cost of living. The amounts shown for January 2026 already include this adjustment.